What if the most significant risk to your financial reporting isn't the five-step model itself, but the professional judgment you apply between those steps? Many practitioners feel a deep sense of uncertainty when they must identify distinct performance obligations or estimate variable consideration under pressure. It's difficult to link theoretical knowledge to the complex scenarios found in professional practice or the rigorous requirements of the ACCA SBR and DipIFR exams. This guide delivers IFRS 15 practical examples for accountants designed to transform that confusion into a structured, professional protection for your organization's financial integrity.

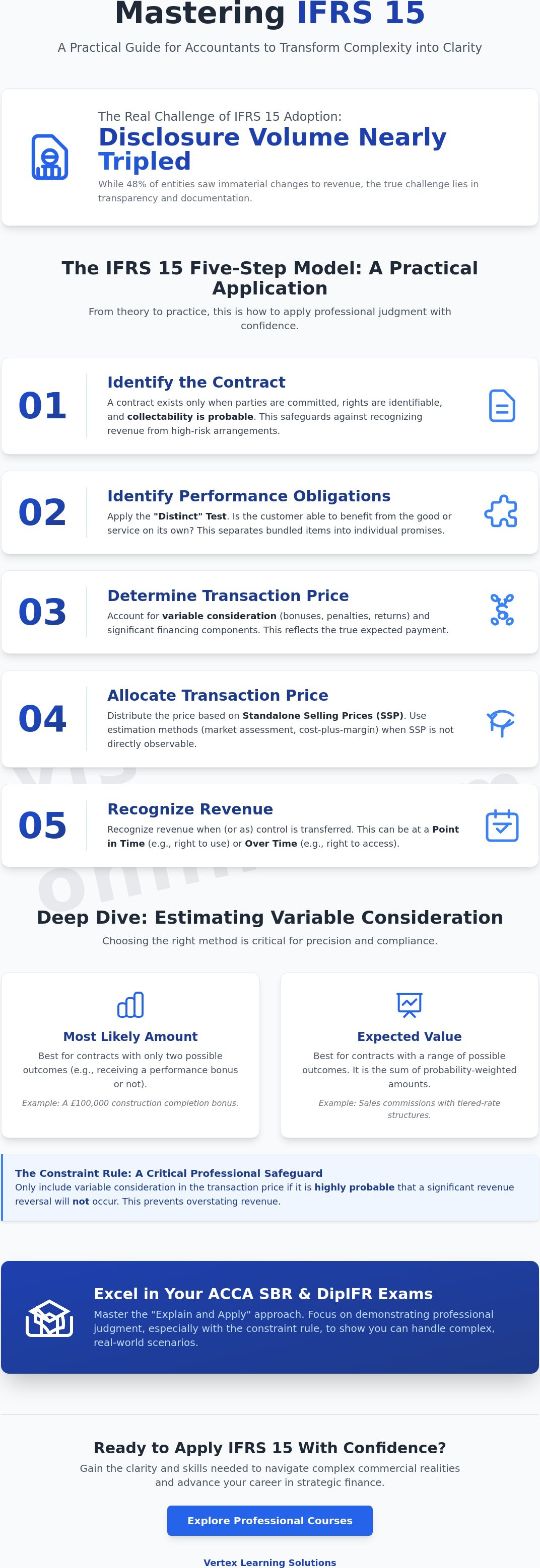

You'll master the nuances of bundled contracts and learn to navigate the 2026 reporting environment with calm authority. Research indicates that while 48% of entities saw immaterial changes to revenue amounts upon adoption, the volume of required disclosures has nearly tripled; this highlights that the true challenge lies in transparency and documentation. We'll examine real-world applications that clarify how to handle bonuses and penalties without compromising precision. This analysis provides a clear roadmap for handling complex commercial realities while preparing you for the presentation shifts introduced by IFRS 18. By the end of this guide, you'll possess the clarity needed to apply IFRS 15 with the same rigor expected in high-level strategic advisory roles.

Key Takeaways

- Master the critical "distinct" test to accurately identify performance obligations, ensuring revenue is only recognized when a customer can benefit from a good or service on its own.

- Navigate complex contracts using IFRS 15 practical examples for accountants to correctly apply the "most likely amount" and "expected value" methods for variable consideration.

- Differentiate between "right to use" and "right to access" in licensing agreements to determine whether revenue should be recognized at a point in time or over time.

- Refine your ACCA SBR and DipIFR exam technique by mastering the "Explain and Apply" approach, focusing on the constraint rule where revenue reversal must be highly unlikely.

The IFRS 15 Five-Step Model: Practical Application Refresher

Mastering revenue recognition starts with moving beyond the mechanical application of rules toward a deep understanding of commercial substance. For a contract to exist under Step 1, it isn't enough to have a signed document; the parties must be committed to their obligations, and collectability must be probable. This initial assessment acts as a professional safeguard, ensuring that revenue isn't recognized when the underlying cash flow is at high risk. Providing IFRS 15 practical examples for accountants often highlights that when commercial substance is lacking, any consideration received is typically recognized as a liability rather than income. For those seeking a foundational IFRS 15 overview, the standard's focus on the transfer of control remains its most defining characteristic.

Step 2: When is a Good or Service "Distinct"?

Determining whether a promise is a separate performance obligation requires the "distinct" test. Consider a software company that sells a perpetual license bundled with a 24-month technical support contract. If the software remains fully functional without the support, the customer can benefit from the license on its own. In this scenario, the license and the support are distinct. However, if the software requires constant, complex updates to remain operational, the two are highly interrelated. This means they'd be treated as a single performance obligation. Professional judgment here is vital. You must decide if the entity is providing a single integrated service or multiple independent goods.

Step 4: Allocation Methods for Accountants

Once the transaction price is determined, including adjustments for non-cash consideration or the time value of money, you must allocate it based on standalone selling prices (SSP). Standalone selling price is the price at which an entity would sell a promised good or service separately to a customer. When an SSP isn't directly observable, accountants use the adjusted market assessment approach or the expected cost plus margin approach. These methods ensure that the allocation reflects what the entity expects to receive for each component. For professionals preparing for the Strategic Business Reporting exam, mastering these allocation techniques is essential for handling the complex, multi-element arrangements frequently tested in the syllabus. Logic and precision in these steps prevent the arbitrary shifting of revenue between reporting periods.

Complex Scenarios: Variable Consideration and Bundled Goods

Variable consideration requires a disciplined approach to estimation. When dealing with bonuses or penalties, you must choose between the "most likely amount" method for binary outcomes and the "expected value" method for a range of possibilities. Consider a construction contract featuring a £100,000 completion bonus subject to weather conditions. If the firm has a high historical success rate on similar projects, the most likely amount might be the full £100,000. However, the constraint rule dictates that you only recognize this revenue if a significant reversal is highly unlikely. This conservative approach prevents "front-loading" profit that could vanish due to unforeseen delays. These IFRS 15 practical examples for accountants demonstrate that the standard prioritizes the reliability of the statement of profit or loss over optimistic projections.

Rights of return are often misunderstood in professional practice. They don't constitute a separate performance obligation. Instead, they represent variable consideration because the final transaction price depends on whether the customer retains the product. You must estimate expected returns and recognize revenue only for the portion unlikely to be returned. This ensures the financial statements reflect the commercial reality of the transaction. If you're looking to solidify your expertise in these areas, the Diploma in IFRS offers the structured framework necessary for such complex judgments.

Accounting for Significant Financing Components

When payments are delayed by more than 12 months, a "hidden" interest component often exists within the contract. You must adjust the promised consideration for the effects of the time value of money. This involves separating the total contract price into revenue from the sale and interest income. Maintaining this distinction is critical for IFRS compliance and ensures the income statement accurately reflects the entity's financing activities. It prevents the distortion of operating margins through financing arrangements.

The Impact of Contract Modifications

Scope changes mid-project require a specific decision: is this a new contract or a cumulative catch-up adjustment? If the additional goods are distinct and the price increases by their standalone selling price, it's a separate contract. If the goods aren't distinct, the modification is treated as part of the existing contract. For those navigating these complexities in high-level roles, understanding specialist accounting qualifications can provide the technical depth needed for such strategic decisions. This level of precision is what separates a standard preparer from a strategic financial partner.

Industry-Specific Recognition: Point in Time vs. Over Time

Deciding whether revenue should be recognized at a single point in time or progressively over time is a cornerstone of professional judgment. These IFRS 15 practical examples for accountants clarify that the distinction often rests on the transfer of control. In the SaaS sector, a "right to use" license is recognized when the customer gains the ability to use the software. Conversely, a "right to access" represents a dynamic service where the customer consumes benefits as the provider performs updates; this requires recognition over time. For customized machinery, if the asset has no alternative use and the entity has an enforceable right to payment for work done, revenue is recognized over time even before delivery.

Construction and long-term projects further complicate this choice. You must select between the "input method," which measures progress based on costs incurred, and the "output method," which focuses on milestones reached. While the input method is common, it requires the exclusion of inefficiencies or wasted materials to maintain accuracy. Selecting the wrong method can lead to significant revenue volatility, which undermines the reliability of your financial reporting. Retailers must also account for loyalty points as a "material right," essentially treating them as a separate performance obligation rather than a simple marketing expense.

Comparison of Recognition Timing

The following table outlines the fundamental differences in recognition patterns across common business models:

| Sector | Recognition Type | Key Criteria |

|---|---|---|

| Retail & E-commerce | Point in Time | Physical transfer of goods and legal title. |

| Subscription Services | Over Time | Customer simultaneously receives and consumes benefits. |

| Customized Manufacturing | Over Time | No alternative use and enforceable right to payment. |

IFRS 15 in the SaaS Sector

Accounting for software requires a precise allocation of the transaction price between implementation fees and monthly subscriptions. If the implementation isn't a distinct service, it's bundled with the subscription and recognized over the contract term. This prevents the artificial inflation of early-period earnings. For students, this is a core component of the Diploma in IFRS. Master these distinctions to ensure your reporting remains beyond reproach. Access our comprehensive training resources to deepen your technical expertise across all reporting standards.

Exam Technique: Passing IFRS 15 Questions in ACCA SBR

Success in the Strategic Business Reporting (SBR) exam requires a shift from rote memorization to high-level application. You shouldn't just state the standard's requirements. Instead, you must adopt the "Explain and Apply" approach. This means identifying the specific principle, such as the transfer of control, and immediately linking it to the transaction values provided in the scenario. Using IFRS 15 practical examples for accountants during your revision helps you recognize how examiners hide complexities within simple-looking contracts. It's the difference between knowing the rule and knowing how to protect the integrity of the financial statements.

A frequent pitfall involves variable consideration. Many candidates correctly identify a bonus or penalty but fail to mention the "highly unlikely to reverse" constraint. Without this specific professional judgment, your answer lacks the technical depth required for a passing grade. You must also consider how IFRS 15 interacts with other standards. For instance, a contract might contain a lease component under IFRS 16 or trigger an onerous contract provision under IAS 37 if costs exceed the expected revenue. Clear, logical links between these standards demonstrate the systemic thinking expected of a strategic professional.

Strategic Business Reporting (SBR) Insights

When structuring a 10-mark answer, use the five-step model as your skeletal framework. Dedicate a brief paragraph to each step, but only if it's relevant to the specific problem. If the issue is purely about identifying performance obligations, don't waste time on Step 5. This focused approach ensures you maximize marks while managing time effectively. For broader strategies on managing this level of the qualification, consult our ACCA Strategic Professional Guide.

Final Checklist for Accountants

Before finalizing any revenue recognition decision, verify these four critical points:

- Does the contract have commercial substance and probable collectability?

- Are the promised goods or services distinct within the context of the contract?

- Has variable consideration been constrained to avoid significant reversals?

- Does the recognition timing reflect the actual transfer of control?

Mastering these nuances ensures your professional judgment remains robust under pressure. Ready to master the numbers? Explore our ACCA SBR Online Course for deep-dive video lectures that bring these IFRS 15 practical examples for accountants to life through expert-led scenarios.

Securing Your Expertise in Revenue Recognition

Mastering revenue recognition isn't merely about memorizing a five-step model; it's about the precision of your professional judgment when commercial realities become complex. Whether you're unbundling SaaS contracts or applying the constraint rule to variable consideration, your ability to link theory to practice is what defines your value as a strategic partner. These IFRS 15 practical examples for accountants provide the technical foundation needed to navigate the 2026 reporting landscape with absolute confidence. As the industry prepares for the presentation shifts of IFRS 18, your mastery of recognition principles remains your most vital professional safeguard.

We're here to provide the expert protection and guidance you need to excel in your professional journey. Our 2026 curriculum offers exam-focused study notes and weekly live sessions specifically designed for SBR students. You'll also benefit from direct, expert tutor support via WhatsApp to ensure no technical nuance remains unclear. Master IFRS 15 with our ACCA SBR Professional Course and transform your technical knowledge into a decisive career advantage. Your path to professional excellence is structured, stable, and fully supported.

Frequently Asked Questions

What is the most common mistake accountants make with IFRS 15?

The most frequent error is the failure to distinguish between a good being "distinct" on its own versus being "distinct within the context of the contract." Many IFRS 15 practical examples for accountants show that while a component might be sold separately elsewhere, it often acts as a mere input to a combined output in a specific agreement. This oversight leads to incorrect unbundling and skewed revenue timing across reporting periods.

How do I distinguish between a contract modification and a new contract?

You distinguish between these by checking if the scope increases due to distinct goods and if the price increases by their standalone selling price. If both conditions are met, you treat it as a new contract. If these criteria aren't satisfied, you treat it as a modification of the original agreement, which usually requires a cumulative catch-up adjustment to revenue already recognized.

Can I recognize revenue if the customer has not paid yet?

Yes, revenue recognition is decoupled from cash receipt and focuses instead on the transfer of control. You can recognize revenue before payment provided a valid contract exists and you've satisfied the performance obligation. However, collectability must be probable at the inception; if there's significant doubt about the customer's ability to pay, the contract fails the Step 1 criteria and revenue shouldn't be recognized.

What is the difference between an input method and an output method?

The input method recognizes revenue based on the entity's efforts, such as labor hours or costs incurred, relative to the total expected inputs. The output method focuses on direct measurements of value transferred to the customer, such as units delivered or milestones reached. You must select the method that provides the most faithful depiction of the transfer of control for that specific commercial arrangement.

How does IFRS 15 handle bundled products and services?

Bundled arrangements require the transaction price to be allocated to each separate performance obligation based on relative standalone selling prices. If a bundle includes a "material right," such as a significant discount on future purchases, that right itself becomes a separate performance obligation. This structured approach ensures that revenue is attributed to the specific period in which the underlying value is actually delivered to the customer.