Most candidates treat financial instruments as a memorization marathon, but IFRS 9 is actually a logical two-step decision tree based on your intent and the contract's terms. It's understandable if you feel overwhelmed by the technical jargon or the shifting regulatory environment, especially with the 2026 amendments addressing ESG-linked features and electronic payment systems. This strategic guide offers IFRS 9 explained for DipIFR students with a focus on providing the professional safety net you need to master the December 2025 and June 2026 exam cycles.

You've likely spent hours struggling to distinguish between FVTPL and FVTOCI or wrestling with the complex math of Expected Credit Losses. We'll simplify these hurdles by providing a clear, structured framework for classification tests and amortised cost calculations. This article breaks down the three-stage impairment model and provides the precise tools needed to handle any financial instrument scenario the examiner presents. We're moving beyond rote learning to ensure you can apply these standards with the rigor and clarity expected of a strategic professional.

Key Takeaways

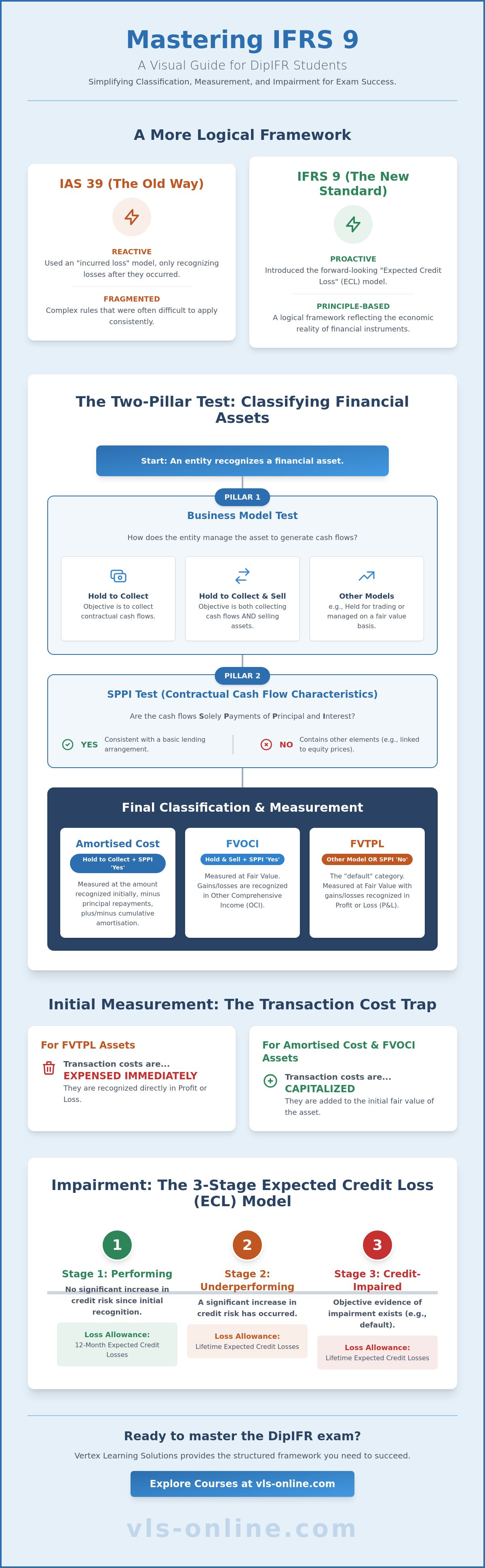

- Understand why IFRS 9 replaced IAS 39 and how its focus on cash flow timing provides a more accurate reflection of financial reality.

- Master the Two-Pillar Test by evaluating the entity's business model and the SPPI criteria to determine asset measurement.

- Gain a clear understanding of IFRS 9 explained for DipIFR students by transitioning from the reactive incurred loss model to the proactive three-stage Expected Credit Loss approach.

- Learn a structured response strategy that involves stating the relevant rule, applying it to specific scenarios, and concluding with precise numerical impacts.

- Simplify the distinction between debt and equity investments to ensure confidence when tackling common DipIFR examination scenarios.

Understanding the Scope and Objective of IFRS 9 in the DipIFR Syllabus

Mastering financial instruments is often the deciding factor for success in the Diploma in IFRS exam. IFRS 9 replaced the older IAS 39 standard to simplify what was once a fragmented approach to accounting for financial instruments. Its primary objective is to ensure that financial statements provide transparent, useful information regarding the timing, amount, and uncertainty of an entity's future cash flows. For those seeking IFRS 9 explained for DipIFR students, it's vital to recognize that the standard isn't merely a set of rules; it's a logical framework designed to reflect the economic reality of financial contracts. This IFRS 9 Overview highlights how the standard moved toward a more principle-based approach, which is exactly what the examiner tests through complex scenarios.

The scope of IFRS 9 is broad. It encompasses financial assets, financial liabilities, and certain contracts to buy or sell non-financial items that can be settled net in cash. A critical point for your exam preparation is the timing of initial recognition. An entity must recognize a financial asset or liability on its statement of financial position at the precise moment it becomes a party to the contractual provisions of the instrument. This rule prevents entities from keeping significant financial commitments off-balance sheet, ensuring a higher level of transparency and risk oversight.

The Three Pillars of IFRS 9

To structure your study effectively, view the standard through three distinct pillars. First, Classification and Measurement determines how we value the instrument on an ongoing basis. Second, Impairment introduces the Expected Credit Loss (ECL) model, which requires a proactive assessment of potential losses. Finally, Hedge Accounting aims to align the accounting treatment with the entity's risk management activities. While hedge accounting is often simplified for the DipIFR syllabus, a solid grasp of the first two pillars is essential for passing the technical components of the exam.

Initial Measurement Principles

At the point of inception, most financial instruments are measured at their fair value, which is typically the transaction price. However, the treatment of transaction costs creates a common trap in exam questions. If an instrument is measured at Fair Value Through Profit or Loss (FVTPL), transaction costs are expensed immediately. Conversely, for assets measured at amortised cost or Fair Value Through Other Comprehensive Income (FVOCI), these costs are capitalized into the initial carrying amount. Understanding this distinction is the first step toward calculating the correct figures in your DipIFR answers.

The Two-Pillar Test: Classifying and Measuring Financial Assets

Once recognition is established, the classification of a financial asset depends on two rigorous criteria. This framework ensures that the measurement reflects both how an entity manages its assets and the nature of the asset's cash flows. For those studying IFRS 9 explained for DipIFR students, mastering this decision tree is non-negotiable for scoring high marks in the financial instruments questions of the exam. The Official IFRS 9 Standard mandates that we evaluate the business model and the contractual cash flow characteristics simultaneously to ensure consistent reporting.

Applying the Business Model Test

The business model assessment isn't about management's intent for a single instrument; it's about how groups of assets are managed together to achieve a specific objective. If the objective is to hold assets to collect contractual cash flows, the asset typically moves toward amortised cost. If the strategy involves both collecting cash flows and selling the assets, Fair Value Through Other Comprehensive Income (FVOCI) becomes the relevant path. Any other model, such as holding for trading or managing on a fair value basis, defaults to Fair Value Through Profit or Loss (FVTPL).

The SPPI (Contractual Cash Flow) Test

The Solely Payments of Principal and Interest (SPPI) test examines whether the cash flows are consistent with a basic lending arrangement. Principal represents the fair value at initial recognition, while interest is consideration for the time value of money and credit risk. A common exam pitfall involves convertible bonds. Because the conversion feature introduces exposure to equity price changes rather than just credit risk, these instruments fail the SPPI test and must be measured at FVTPL. If you're finding these technical distinctions challenging, our DipIFR preparation materials provide additional drill-down scenarios to build your professional confidence.

For equity instruments that aren't held for trading, IFRS 9 allows an irrevocable election at initial recognition to present subsequent changes in fair value in OCI. It's a strategic choice that prevents profit or loss volatility, though it's important to remember that these gains are never recycled to the income statement. This election is often a focal point in exam scenarios where a company holds long-term strategic investments in other entities.

Navigating Impairment: The Expected Credit Loss (ECL) Model Simplified

The transition from the incurred loss model of IAS 39 to the Expected Credit Loss (ECL) model of IFRS 9 represents a fundamental shift in accounting philosophy. Under the old regime, losses were only recognized when a trigger event occurred, often resulting in "too little, too late" provisions. For those seeking IFRS 9 explained for DipIFR students, the key is understanding that we now recognize losses before they happen, using forward-looking information. This IFRS 9 Summary and Guidance provides an excellent breakdown of how this proactive approach stabilizes financial reporting during economic volatility by requiring entities to account for credit risk from the moment an asset is recognized.

The General Approach (The Three Stages)

The general model categorizes financial instruments into three stages based on the change in credit risk since initial recognition. This structure ensures that the level of loss recognized is proportionate to the risk exposure:

- Stage 1: Includes assets with no significant increase in credit risk. You recognize a 12-month ECL, representing the losses from default events possible within the next year.

- Stage 2: Triggered by a Significant Increase in Credit Risk (SICR). You must recognize lifetime ECL, covering all possible default events over the life of the instrument.

- Stage 3: The asset is credit-impaired. You recognize lifetime ECL and calculate interest revenue on the net carrying amount (carrying amount less the loss allowance).

Simplified Approach for DipIFR

Exam scenarios frequently feature trade receivables that don't contain a significant financing component. In these cases, IFRS 9 mandates a simplified approach, allowing entities to skip the three-stage assessment and always recognize lifetime ECL. This is typically achieved using a provision matrix, which applies historical loss rates to different age bands of receivables while adjusting for future economic conditions. If you want to master these calculations for your exam, consider enrolling in our comprehensive DipIFR course to practice with exam-style provision matrices. This method ensures that credit risk is reflected immediately, providing the professional protection and transparency regulators demand.

Exam Technique: How to Tackle IFRS 9 Questions in the Diploma in IFRS

Success in the Diploma in IFRS exam requires more than technical knowledge; it demands a structured, professional approach to answering complex scenarios. When you encounter a financial instruments question, follow a rigorous "Rule, Apply, Conclude" framework. Start by stating the relevant accounting principle clearly. A high-impact, mark-earning sentence like "Classification depends on the entity's business model and the SPPI test" immediately demonstrates your technical command to the examiner. This guide provides IFRS 9 explained for DipIFR students with a specific focus on converting theoretical understanding into maximum marks during the 2026 exam sittings.

Distinguishing between debt and equity investments is a recurring theme in DipIFR papers. While debt instruments can be measured at amortised cost, FVTOCI, or FVTPL based on the two-pillar test, equity instruments must always be measured at fair value. Mastering the effective interest rate table is essential for any debt instrument measured at amortised cost. Ensure your table includes the opening balance, interest income at the effective rate, cash received (coupon rate), and the closing balance. Precision in these calculations provides the foundation for the numerical conclusions that examiners look for in high-scoring scripts.

Common Pitfalls and How to Avoid Them

One frequent error is the treatment of transaction costs. Remember that for instruments measured at FVTPL, transaction costs are expensed immediately, whereas they are capitalized for other categories. Another common mistake is attempting to classify equity investments at amortised cost, which is never permitted under the standard. To refine your application of these rules, check out our Diploma in IFRS online training for guided practice on past exam scenarios.

Final Revision Checklist for 2026

As you prepare for the 2026 exams, pay close attention to reclassification rules. Although reclassification of financial assets is rare and only occurs when the business model changes, it carries significant mark potential. Additionally, practice 15-mark consolidated questions where financial instruments often create the most complexity in the statement of financial position. For those looking to advance their expertise beyond the diploma level, you can learn more about ACCA Strategic Business Reporting for advanced IFRS 9 topics and their impact on group financial statements.

Strategizing for Success in the 2026 DipIFR Exams

Mastering financial instruments requires a deliberate shift from rote memorization to logical, principle-based application. You've explored the core decision-making frameworks, from the dual-pillar classification tests to the forward-looking Expected Credit Loss model. This systematic approach ensures you aren't just calculating figures; you're providing the high-level professional insights that examiners demand. With IFRS 9 explained for DipIFR students through this structured lens, the technicalities of the 2026 syllabus become a manageable strategic advantage rather than an overwhelming hurdle.

We offer the professional safety net and expert guidance needed to navigate these complex regulations with absolute confidence. Our curriculum is designed to simplify complexity while maintaining the highest standards of professional integrity and precision. Master IFRS 9 with our Expert-Led DipIFR Course, which includes weekly live interactive sessions and direct tutor support via WhatsApp. Combined with our exam-focused study notes for 2026, you'll have every tool required to secure your qualification. Your professional progression is a strategic investment, and we're committed to ensuring your success is both predictable and stable.

Frequently Asked Questions

What is the difference between FVTOCI and FVTPL?

The primary difference lies in where the fair value fluctuations are reported in the financial statements. FVTPL requires all gains and losses to be recognized immediately in the profit or loss account; this is the default for trading assets. FVTOCI is reserved for debt instruments held to collect and sell or for strategic equity investments where an entity elects to avoid profit volatility by reporting changes in other comprehensive income.

When should transaction costs be capitalized under IFRS 9?

Transaction costs are capitalized when a financial instrument is measured at amortised cost or Fair Value Through Other Comprehensive Income. In these cases, costs like legal fees or stamp duties are added to the initial carrying amount of the asset. However, if the instrument is classified as Fair Value Through Profit or Loss, these costs must be expensed immediately to ensure the initial measurement reflects current market value.

What are the criteria for the SPPI test in DipIFR exams?

The SPPI test requires contractual cash flows to consist of solely payments of principal and interest on the principal amount outstanding. For this IFRS 9 explained for DipIFR students section, remember that "interest" must only compensate for the time value of money and credit risk. If a contract includes features like conversion into equity or leverage, it fails this test and necessitates a fair value through profit or loss measurement.

Does IFRS 9 apply to both financial assets and liabilities?

IFRS 9 provides a comprehensive framework for both financial assets and financial liabilities. While the classification of assets follows the business model and cash flow tests, liabilities are typically measured at amortised cost. Entities may designate liabilities at Fair Value Through Profit or Loss only if it eliminates an accounting mismatch or if the liability is part of a group managed on a fair value basis.

How is amortised cost calculated using the effective interest method?

Amortised cost is determined by applying the effective interest rate to the opening carrying amount of the instrument. This methodical approach involves adding the calculated interest income to the opening balance and then subtracting any cash payments received. This ensures the IFRS 9 explained for DipIFR students context remains focused on the effective yield rather than the nominal coupon rate, reflecting the true economic return over the asset's life.