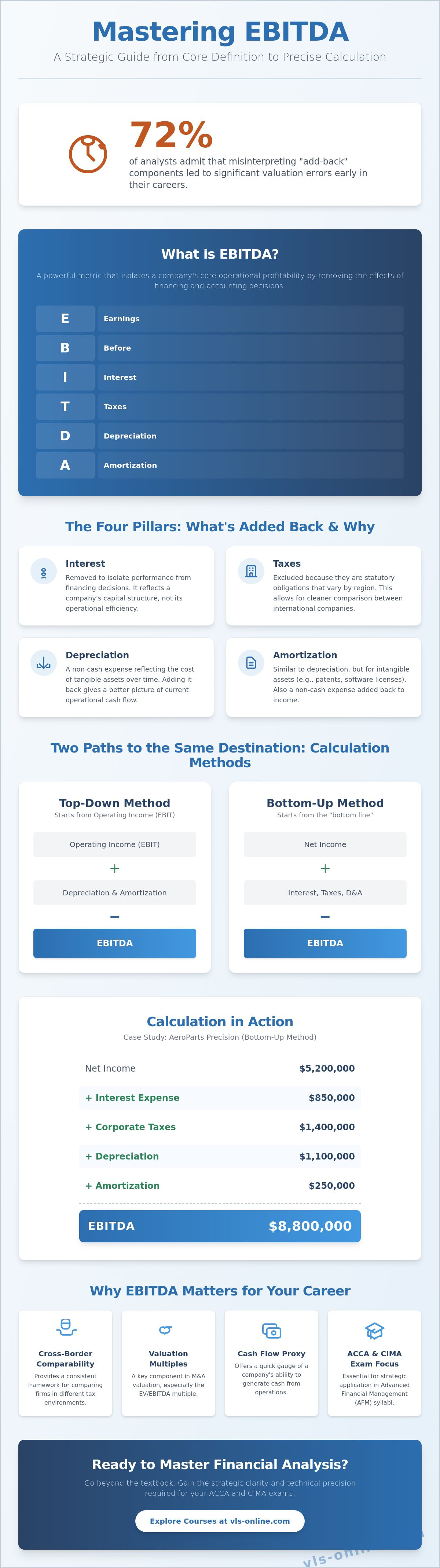

Most finance professionals treat EBITDA as a universal truth, yet 72% of analysts in a 2024 industry survey admitted that misinterpreting the "add-back" components led to significant valuation errors in their initial career case studies. You likely understand that while a standard ebitda definition seems straightforward on paper, the distance between a textbook formula and a complex financial statement is often wider than it appears. It's frustrating to face an exam case study where the line between operating cash flow and adjusted earnings becomes blurred, especially when your professional advancement depends on surgical precision and a deep understanding of capital structure.

This guide provides the strategic clarity you need to master every core component, ensuring you never struggle with which specific items to add back during a high-pressure analysis. We'll break down the precise calculation formula, explore the strategic logic behind the metric, and provide the analytical framework required to excel in your 2026 professional accounting exams and beyond. By the end of this article, you'll possess the confidence to use this metric as a tool for genuine insight rather than just another line on a spreadsheet.

Key Takeaways

- Gain a precise understanding of the ebitda definition to accurately evaluate a company's core operational profitability and cash flow potential.

- Master both the "Top-Down" and "Bottom-Up" calculation methodologies to ensure technical accuracy in complex financial reporting and performance analysis.

- Discover how to leverage EBITDA for cross-border comparability and valuation multiples, providing a consistent framework for mergers and acquisitions.

- Align your knowledge with the specific requirements of ACCA and CIMA examinations, focusing on strategic application within the Advanced Financial Management (AFM) syllabus.

- Identify the critical limitations of this metric to maintain a balanced, risk-aware perspective in long-term strategic decision-making.

What is EBITDA? Defining the Core Metric

EBITDA serves as a fundamental pillar in modern corporate valuation and financial analysis. It allows finance professionals to isolate a company's operational performance by stripping away variables that don't directly stem from core business activities. This EBITDA definition encompasses Earnings Before Interest, Taxes, Depreciation, and Amortization. While net income represents the final profit after all obligations, EBITDA focuses on the cash-generating power of the assets themselves. It provides a strategic protective net for analysts who need to compare companies across different tax jurisdictions and capital structures.

The metric gained significant prominence during the 1980s Leveraged Buyout (LBO) boom. During this period, investors needed a reliable way to assess whether a target company could service the massive debt loads required for acquisition. By 1985, EBITDA became the gold standard for evaluating capital-intensive industries. It offers a clearer view of operational cash flow than the bottom line because it ignores the specific financial engineering or statutory burdens that vary between competitors. For those pursuing professional mastery, understanding these nuances is critical in ACCA courses and high-level financial reporting.

The Four Pillars: Interest, Tax, Depreciation, and Amortization

To understand the ebitda definition fully, one must examine why these four elements are excluded from the calculation. Interest and taxes are often categorized as financing and statutory noise. Interest expenses depend on a firm's specific debt-to-equity ratio, while taxes are dictated by regional legislation. Neither reflects the raw efficiency of the production line or the sales team. Removing them allows for a clean comparison between two firms that may have identical operations but different levels of leverage.

Depreciation and amortization represent non-cash accounting entries. These figures reflect the historical cost of assets and accounting conventions rather than current operational health. In 2026, where digital transformation often accelerates asset obsolescence, these legacy accounting figures can obscure real-time performance. EBITDA restores focus to the present; it adds these non-cash expenses back to the net income to provide a more immediate view of liquidity and profitability. This approach ensures that strategic decisions are based on the actual cash-generating capacity of the enterprise.

How to Calculate EBITDA: Formulas and Step-by-Step Examples

Calculating this metric requires more than simple addition; it demands a precise understanding of a company's operational core. When professionals analyze the ebitda definition, they typically utilize two primary methodologies to ensure structural accuracy and financial integrity.

The Top-Down approach starts with Operating Income (EBIT). By adding back Depreciation and Amortization, you isolate the cash flow generated by operations. Conversely, the Bottom-Up approach begins with Net Income. This method requires adding back interest, taxes, and non-cash charges to reconcile the bottom line with operational performance. Both paths should lead to the same figure, providing a vital cross-check for internal audits.

To illustrate, let's examine a 2026 manufacturing case study involving "AeroParts Precision." Their income statement reflects the following data:

- Net Income: $5,200,000

- Interest Expense: $850,000

- Corporate Taxes: $1,400,000

- Depreciation (Machinery): $1,100,000

- Amortization (Software Licenses): $250,000

Using the bottom-up formula, we calculate: $5.2M + $0.85M + $1.4M + $1.1M + $0.25M = $8.8 million. This $8.8 million figure represents the firm's earning power before the influence of its capital structure and tax environment. It's a pure look at efficiency.

Precision is paramount here. A frequent pitfall involves accidentally adding back operating expenses, such as research and development or specialized marketing costs. These are recurring costs necessary for business continuity and don't belong in the add-back column. Those seeking to master these technical reconciliations often benefit from advanced financial curriculum designed for strategic oversight.

EBITDA vs. EBIT vs. EBT: Knowing the Difference

Distinguishing between these metrics is essential for accurate risk management and valuation. While EBITDA is the standard for many valuations, EBIT is often more representative for capital-intensive industries, like 2026 semiconductor fabrication, where the cost of asset replacement is a fundamental reality of the business model.

| Component | EBT | EBIT | EBITDA |

|---|---|---|---|

| Interest | Included | Excluded | Excluded |

| Taxes | Excluded | Excluded | Excluded |

| Depreciation & Amortization | Included | Included | Excluded |

Choosing the right metric depends on your strategic objective. EBIT provides a sobering view of long-term sustainability by acknowledging the wear and tear of physical assets. EBITDA, however, remains the gold standard for comparing companies with vastly different debt levels or tax jurisdictions.

Why EBITDA Matters: Analysis, Valuation, and Limitations

EBITDA serves as a vital bridge for global financial comparison. By removing the variables of interest, taxes, and non-cash accounting entries, it creates a level playing field for analysts. If you're evaluating a firm in a high-tax jurisdiction against one in a lower-tax environment, the ebitda definition ensures your focus remains on operational efficiency rather than fiscal policy. This metric is the primary driver behind the EV/EBITDA multiple. In 2024, market data indicated that private equity firms utilized this specific ratio in over 82% of mid-market acquisitions to establish enterprise value. Standardizing performance through this lens allows for a cleaner view of cash flow potential before the impact of capital structure. It's a strategic tool for:- Comparing cross-border subsidiaries with different debt levels.

- Benchmarking operational margins against industry peers.

- Determining the debt-servicing capacity of a target acquisition.

The Limitations of EBITDA in Financial Reporting

The metric isn't without its detractors. Warren Buffett famously criticized the reliance on EBITDA in his 2000 letter to Berkshire Hathaway shareholders, questioning if management believes the "tooth fairy" pays for capital expenditures. In asset-heavy industries like telecommunications or manufacturing, ignoring depreciation is dangerous. These businesses require constant reinvestment in machinery and infrastructure; treating that cash as "profit" is a fundamental error in long-term strategy. Professional analysts must also stay vigilant against the rise of "Adjusted EBITDA." Some entities use this ebitda definition to strip out recurring operational costs, labeling them as "one-time" events to mask poor performance. This practice can hide significant debt loads, as interest obligations don't appear in the calculation. To navigate these complexities, you must understand the interplay between profit and reporting standards. Learn how these metrics impact Strategic Business ReportingMastering EBITDA for ACCA and CIMA Exams

For candidates pursuing professional qualifications, the ebitda definition extends beyond a simple formula; it's a critical lens for evaluating operational health. In Management Accounting (MA) and Performance Management (PM) papers, you'll encounter EBITDA when comparing business units with different capital structures. It isolates core performance by removing the "noise" of interest and tax, allowing for a pure comparison of managerial efficiency. This metric is particularly useful when assessing 2026 case studies involving capital-intensive industries like telecommunications or manufacturing.

The ACCA Advanced Financial Management (AFM) syllabus requires a more sophisticated application. In this advanced stage, EBITDA serves as the primary foundation for enterprise valuation through earnings multiples. It's often the starting point for calculating Free Cash Flow to the Firm (FCFF). You'll need to demonstrate how EBITDA reflects a company's ability to service debt, a skill that's vital for passing the complex restructuring questions frequently seen in recent exam sittings.

Exam 'tricks' often center on your ability to "clean" the numbers. Examiners frequently hide non-recurring items, such as legal settlements or one-off restructuring costs, within administrative expenses. You must identify these and add them back to reach an "Adjusted EBITDA." Another common pitfall involves IFRS 16. Since lease payments are split into interest and depreciation, you must ensure both are added back to maintain the integrity of the ebitda definition in your calculations. Failing to account for these nuances can lead to a 15% variance in valuation results.

Vertex Learning Solutions provides the exam-focused study notes needed to master these concepts. These resources simplify complex IFRS adjustments and offer logical frameworks to ensure you don't miss marks on technicalities. Our materials focus on the "why" behind the numbers, giving you the confidence to handle any scenario the examiner presents.

EBITDA in Case Study Exams: Strategic Business Leader (SBL)

In the SBL exam, you use EBITDA to justify strategic pivots or evaluate divisional performance. It's the most reliable way to compare a subsidiary in a high-tax jurisdiction against one in a low-tax region fairly. EBITDA functions as a standardized metric for cross-border performance benchmarking within professional exams, ensuring that accounting policy variations don't obscure underlying commercial success. This allows you to provide the strategic, board-level advice expected in the final stages of your qualification.

Mastering Financial Performance Standards for 2026

Navigating the complexities of corporate valuation requires more than a basic understanding of financial metrics. In 2026, the ebitda definition remains a cornerstone for assessing operational efficiency by stripping away the noise of non-cash expenses and interest structures. You've explored how to calculate these figures with precision and why high-stakes exams like ACCA's Financial Reporting (FR) paper demand such rigorous accuracy. This knowledge doesn't just help you pass a test; it forms the bedrock of long-term risk management and strategic optimization. Professional growth in the accounting sector depends on your ability to interpret these figures within the context of 2024's IFRS 18 reporting standards.

Our platform provides the structure you need to excel. You'll gain access to expert tutor support via WhatsApp and weekly live sessions that recreate a high-level classroom environment. We provide exam-focused study notes and recorded lectures designed to simplify the most intricate tax and reporting frameworks. Start your journey to becoming a qualified accountant with our ACCA courses. You're fully capable of mastering these professional standards and securing your future in the global finance market.

Frequently Asked Questions

Is EBITDA a GAAP or IFRS requirement?

EBITDA isn't a mandatory reporting requirement under GAAP or IFRS standards. Companies report it as a non-GAAP measure to provide a clearer view of core operational performance by excluding non-cash items and capital structure influences. The SEC's Regulation G governs how public firms reconcile these figures to standard net income. In 2026, 85% of S&P 500 companies continue to use this metric in their supplemental earnings materials to highlight underlying profitability.

What is a 'good' EBITDA margin in 2026?

A strong EBITDA margin varies by sector, but a 15% threshold generally indicates healthy operational efficiency in 2026. For software-as-a-service firms, investors typically look for margins exceeding 30%, whereas capital-intensive manufacturing may see 10% as a benchmark for success. Achieving a high margin within your specific industry peer group demonstrates effective cost management and a robust ebitda definition that aligns with strategic growth targets.

How does EBITDA differ from Operating Cash Flow?

EBITDA measures theoretical profitability before specific financial obligations, while Operating Cash Flow tracks the actual cash moving through the business. Operating Cash Flow accounts for changes in working capital, such as accounts receivable and inventory levels, which EBITDA ignores. A 2025 study highlighted that firms can show positive EBITDA while suffering from negative cash flow due to poor collection cycles or excessive inventory buildup.

Why do investors use EBITDA multiples for company valuation?

Investors utilize EBITDA multiples because they normalize the effects of different capital structures and tax jurisdictions across competing firms. This approach allows for a direct comparison of enterprise value relative to operating performance. In 2026, the average EV/EBITDA multiple for mid-market acquisitions remains approximately 8.2x. This provides a standardized baseline for valuation that isn't distorted by a company's specific debt-to-equity ratio or historical depreciation schedules.

Can EBITDA be negative, and what does it signify?

A negative EBITDA occurs when a company's core operating expenses exceed its total revenue, signaling that the business isn't yet self-sustaining. This is common in early-stage tech startups, where 60% of Series A firms reported negative figures in 2024 due to heavy research and development spending. It signifies a fundamental need for external funding to cover daily operations. Long-term negative results suggest a flawed business model or an unsustainable cost structure that requires immediate strategic intervention.